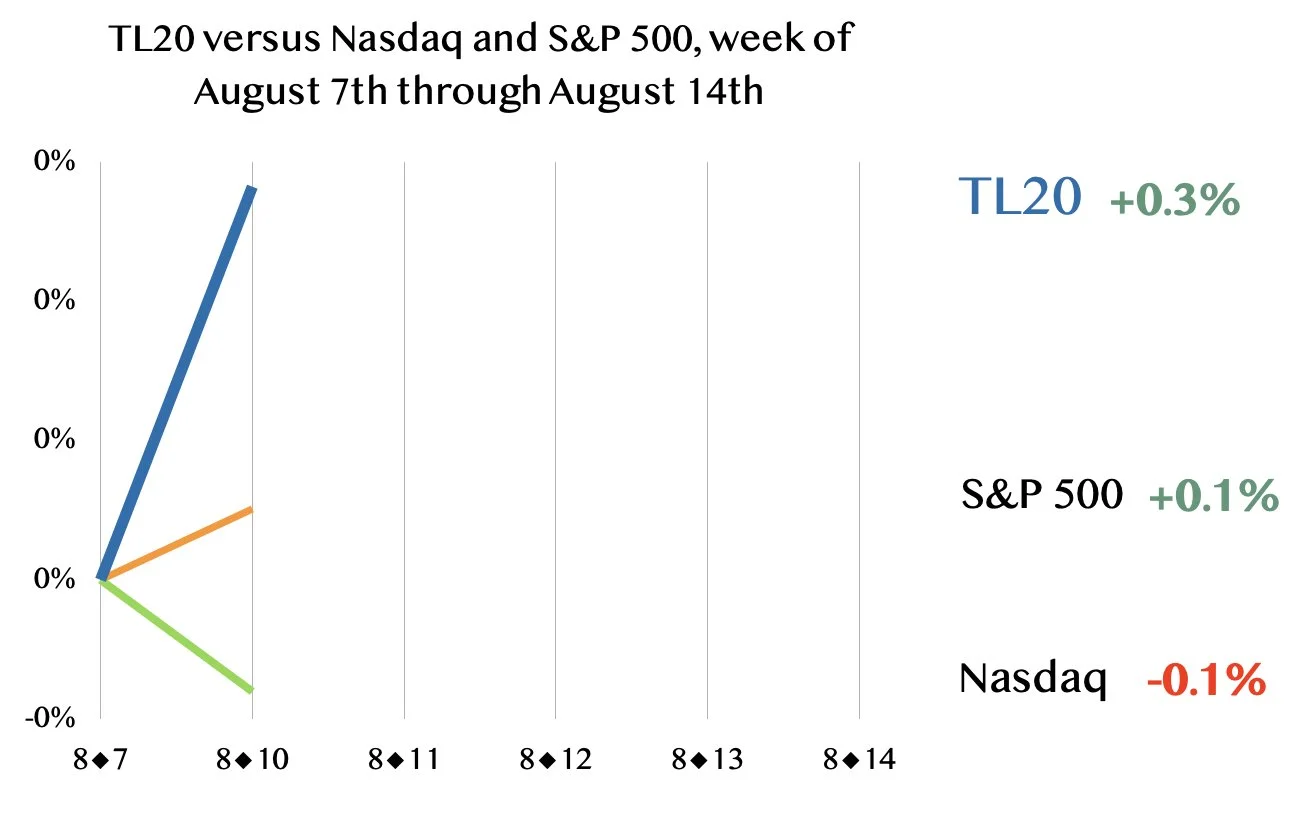

TL20 leads benchmarks

Year-to-date, the TL20 group of stocks to consider is up fifty-four percent, better than the fifteen-percent gain of the Nasdaq and the thirteen-percent gain of the S&P 500. Read about the TL20

TL is just $1 a week for the first four weeks

I’ve thought a lot this year about what happens if all the plans for artificial intelligence investment fail to show up. What if the financing doesn’t come through as expected? What do AI companies do if they build data centers and they can’t sell all the capacity? What happens to the chip makers if they suddenly find orders being cancelled?

It’s refreshing to talk with Paddy Srinivasan, CEO of software maker DigitalOcean. He’s contemplated the negative scenarios as well, and he admits there are “known unknowns.”

“There will be a 1999,” Srinivasan observed in a chat he and I had via video last week. “Now, how do we survive that?” He was alluding to the plunge in the Nasdaq Composite as the DotCom bubble burst. (Actually in March of 2000, but the reference is clear.)

“Are we in 1998 today or are we in 1996? Nobody knows, right?”

Rather than “party like it’s 1999,” Srinivasan has been performing what amounts to a delicate balancing act. He is both courting the whales, such as software startup Courser (in the process of being acquired by SpaceX for $60 billion), while also avoiding being dependent on them by building an enduring base of smaller customers who come for continually increasing capabilities in AI.

Thursday evening was a good one for multiple software names, mostly of the programming tool or infrastructure sorts, as you can see from the table at the bottom of this post, in which I’ve highlighted the software stocks in blue. The average return of software names following their report this week is 9%, better than the 6% average for all stocks reporting.

Bear in mind, I’m still tabulating!

Among names surging Friday morning are Twilio, whose CEO I interviewed last night; and JFrog, which sells tools to check the quality of programming code, is one of the vendors that was hit the hardest back in February when Anthropic’s Claude Code Security debuted and seemed like it would mean the end of all traditional coding tools.

Shares of software maker Twilio are surging by 16% in late trading Thursday, at $225, as the company once again hit milestones in CEO Khozema Shipchandler’s pledge to boost the company’s growth and profitability.

Revenue growth keeps rising, up 22% last quarter versus 13% growth a year ago, the company reported this evening. And the free cash flow margin continues to expand, reaching 24% last quarter versus 21% a year earlier.

Shipchandler was kind enough to talk with me following the report as he has done six times previously. (See the sidebar.)

What’s clear to me is that Shipchandler has an opportunity to expand the company’s offerings in artificial intelligence now that he has stabilized and vastly improved the company’s financials.

“It’s very early days that, you know, but we have aspirations in governance and observability” of AI programs, says Shipchandler.

The AI “token” disaster I wrote about in May is hitting companies hard — specifically, hitting their budgets really hard, according to Yamini Rangan, the CEO of front-office software maker Hubspot.

Her company’s stock is plummeting Thursday morning after the company’s Wednesday evening earnings report came up short because companies are trying to control runaway AI budgets and getting pickier as they do so.

This is one of the biggest concerns I’ve had about the software group: not that they would be made obsolete but that so much distraction would emerge from the whole AI push inside of corporations that it would destabilize the traditional commercial software market. We’re seeing that play out now.

WHY SANDISK WILL BE OKAY

Among the AI-linked names, few have had as rich a year as Sandisk, makers of NAND flash memory chips, whose stock is up 469% this year at Wednesday’s close of $1,350.50. However, the shares are down 11% this morning after the company’s revenue forecast Wednesday evening came up shy of consensus at $10.55 billion versus $10.8 billion. This is the first time the company has disappointed with its revenue outlook since it came public in February of last year as a spin-off of Western Digital.

In addition to SpaceX’s very mixed report Tuesday evening, earnings results overnight featured continued strength from Advanced Micro Devices and Arista Networks, and some surprising positives for the software group, including Shopify, Kaltura, Dynatrace, while other software makers that have already been under pressure, such as Criteo and CS Disco plummeted.

Dynatrace, one of the tools vendors in “DevOps” that I highlighted in this week’s podcast, is having a better time today than back in May.

With Dynatrace, we now have two of the five names I mentioned on the podcast, including DigitalOcean, yesterday, delivering positive results.

AMD shares are down six points at $487.30 despite a very strong report. The shares had been up 142% since the start of the year, so, I regard this really as profit-taking and nothing to do with any issues in AMD’s business, which continues to get stronger and stronger.

Tuesday, the day of SpaceX’s first quarterly report as a public company, was a funny trading day. The stock gained 9% in regular trading, lifted by the overall positive attitude about all things AI, to about $125. But then it gave up 8% in after-hours as the report came out, retreating to $115 and change and continuing to trail the offer price of $135 of the June initial public offering.

The stock continued to fall this morning, down 11% at $111.07.

The headline is that the company beat expectations. The key element, however, for many, is capital spending that came in a lot hotter than expected, and looks set to go much higher from here.

Palantir shares are seeing the biggest after-hours/pre-market gain since February of last year, up 15% at $144.45 following on Monday evening’s report, and estimates and prices targets are likely headed higher Tuesday.

The company beat on every metric that mattered to the bullish types, results that are unique in the software industry.

My sense is Palantir is being helped as investors trade out of AI competitor SpaceX, whose shares have lost a third of their value since the IPO in June. SpaceX was likely direct competition for Palantir shares, and the movement of money into SpaceX stock doubtless contributed to a 29% drop in Palantir leading up to this afternoon’s report. I sense the curse of SpaceX has now lifted from Palantir, allowing investors to focus on the fundamentals.

We’re past the heaviest two weeks of earnings, but we have tons more reports to come. The cloud giants, Amazon, Microsoft, and Alphabet, have signaled continued spending even as their backlog swells, providing support for the AI trade. Software companies have turned in a very mixed performance, with cyber-security being the one bright spot. This week features the traditionally most expensive stocks in tech such as Palantir and Astera Labs, but also the tools makers that are riding the AI wave such as Datadog and Digital Ocean. And, special mention of AXT, whose wafer sales are a remarkable new chapter in its forty-year history.

Thursday evening’s earnings have prompted a jump in late trading of 11% in shares of Amazon and a drop of 8% for Apple, which is not surprising as I see Amazon one of the best positioned Mega Caps for AI along with Alphabet’s Google, while Apple has a mess on its hands with the rising cost of memory chips affecting iPhone and Mac costs and pricing, an issue that I expect to linger.

The evening also contained some interesting surprises that tend to reinforce the AI trade.

The biggest gainer after-hours is forty-year-old semiconductor company AXT of Fremont, California, up 37% in early Friday trading at $65.25

AXT makes the wafers that are used to make chips.

Tonight’s revenue upside of 39%, $48 million against a Street forecast for $34 million, is the biggest upside in at least five years, according to FactSet

The New York Times’s Rob Copeland on Thursday reported that hedge fund Situational Awareness has suffered a massive collapse in its AI-linked investments and had to be rescued by hedge fund Citadel, which swooped in to buy $10 billion of Situational’s stock holdings at “a substantial discount,” citing multiple unnamed parties.

The move was apparently prompted by gigantic declines of stocks held by Situational. The fund had enormous leverage, Copeland relates, so that the stock drops were amplified, prompting margin calls the firm couldn’t meet.

I never actually looked into Aschenbrenner’s investments. These are not, in my mind, the most promising firms to own in AI. They are mostly in the commodity business of renting GPUs to all comers.

On Wednesday evening’s conference call with Microsoft CEO Satya Nadella, we learned that Nadella has been reading one of the noteworthy business books of the year, “1873,” by Liaquat Ahamed. The book is about the speculative railroad building of the 1800s, and it’s very timely as it talks about excesses, credit bubbles, and what happens when it all comes crashing down — the very issues that hang over the artificial intelligence boom in which Microsoft is participating along with other tech giants.

Nadella brought up the book in response to a question by Bernstein analyst Mark Moerdler, who wanted to know “How does Microsoft protect itself if there really is overcapacity and overbuilding of data centers or overbuilding of chips?”

Said Nadella, “All of us are reading this 1873 as the book to be read,” said Nadella. What he’s learned, however, from the book, seems to miss Ahamed’s point, and didn’t really answer Moerdler’s question. “You’ve got to run an efficient railroad,” said Nadella, which is not really the point of the book. The point is the entire world inefficiently allocated capital for a period of 25 years. “I think you've got to get the product shape right,” added Nadella, which is what a product manager says when they have no answer for a really big question.

Tuesday evening was another very mixed bag for the AI trade, with shares of chip equipment maker KLA down 6% in late trading, and data center power supplier Vertiv down 12% in early Wednesday trading. But two other TL20 stocks to consider did very nicely, Seagate and Bloom Energy, their shares surging after-hours.

If I had to sum it up, I would say that the very focused product portfolios of Bloom and Seagate — a fuel cell, a hard drive — make for very clean reports, while the diversity of the businesses at KLA and Vertiv mean there are more “moving parts” every quarter, if you will, which makes it harder for the results to always satisfy the Street.

Bloom, maker of fuel cells that convert hydrogen and natural gas into energy to power data centers, continues to be a runaway train of sorts. The company’s reported revenue for the quarter came in 29% above consensus, at $1.07 billion, the seventh quarter in a row of higher-than-expected sales.

We continue to be in the unwind of the artificial intelligence trade. There’s no fundamental reason other than the stocks had “gone parabolic” from April through June, and it was time for them to come back to earth.

The TL20 group of stocks to consider is a good barometer of that AI trade with names such as Vertiv and Micron Technology.

The most interesting question coming out of last week’s reports is, Are investors rotating in a meaningful way from chips into software stocks.

The first batch of earnings are in for the week, and the result is punishment for stocks that had risen sharply this year and have failed to meet high expectations, including glass and fiber-optics giant Corning, down 16% at $116.32, and chip maker Amkor, down 24% at $46.35.

What you’re seeing with today’s losers is that revenue expectations had gotten ahead of reality based on exuberance about the current business environment, and now that’s being corrected. Business is still fundamentally healthy for these companies, but not always as big as some would like.

You’re also seeing the continued unwind of the AI trade given substantial investor anxiety about how much is sustainable in massive data center build-outs.

I have been skeptical of artificial intelligence being successful in the enterprise because of the enormous complexity of using AI to engineer something that is of acceptable quality. On Monday, analyst Rishi Jaluria of RBC Capital provided some excellent data that reinforces my skepticism.

It’s a delightful piece of work, one of the most enjoyable I’ve come across in a while. I don’t know if it will change investors’ minds, but it’s worth pondering.

Jaluria offers a “model,” or, as he puts it, a “formal framework, which investors can scrutinize and battle-test,” which incorporates the typical cost of commercial software and the hypothetical cost to build stuff with AI to equal or replace the commercial stuff.

Jaluria compared what it costs to build an AI app versus buying one from Hubspot, Microsoft and other established software vendors. His conclusion is that the “total cost of ownership,” TCO, of making something from AI is not worth it.

The week ahead is ferociously busy for earnings with Apple, Meta, Amazon and Microsoft and other tech giants, but also interesting for a host of lesser-known companies.

The table at the bottom of the post features ninety-one companies — ninety-one! — reporting earnings this week. Hey, if they ever change the rules for quarterly disclosure, this might be one of your last times to pig out on such a buffet.

I expect to hear bad news from Apple, Amazon, Microsoft and Meta. Apple is grappling with the rising cost of DRAM, with its attempts to secure the U.S.’s approval of purchase of DRAM chips from China’s CXMT still very much in the headlines. Microsoft and Meta will likely, similar to Alphabet last week, be in the penalty box for their skyrocketing capital spending plans.

For others, such as Reddit and Coursera, the story will be a mixed bag of whether they can survive the erosion of AI of their content business. Reddit reports Thursday evening.

Consider instead several of the more interesting names, most under a trillion dollars in market cap.

This first full week of earnings reports showed what looks like a turn away from the semiconductor beneficiaries of the artificial intelligence trade and toward the beleaguered software group.

Shares of TE Connectivity, Texas Instruments, MaxLinear, Intel, and BE Semiconductor, all of which had very favorable reports, sold off hard. All three had been up by a huge amount this year prior to their reports, as you can see from the table below.

Google also sold off hard despite robust results reported Wednesday evening.

Conversely, software makers SAP, RingCentral, VeriSign and Wex all had significant gains after trailing the market this year.

Thursday was a banner day for followers of the microprocessor trade, with Intel reporting results after market close and Advanced Micro Devices holding what has become an annual affair in San Francisco, its update on its artificial intelligence chips.

Intel initially spiked double-digits in late trading, but gave up some gains but is up just 2% in early Friday trading, at $102.87. AMD shares traded down two points during Thursday’s regular session.

The key for Intel still is the “foundry” business, bringing in outside customers to use Intel’s factories.

The song remains the same at Intel, in a sense: Going back in time to the Gelsinger days, Intel has always had interested parties, and never found a large customer. In years past, the PDK simply didn’t deliver the goods. Hopefully, with Tan’s rigor, and the sense of opportunity, this 14A will be the real deal. We may know in October.

With turmoil over Chinese AI models, worries about AI infrastructure’s private credit market exposure, and persistent questions about return-on-investment of massive spending, it was no surprise the Street spent all of Wednesday evening peppering Alphabet’s Google’s CEO, Sundar Pichai, and CFO, Anat Ashkenazi, about all those things.

It sounded to me like no one got a straight answer about any of it. As a result, Alphabet shares sold off by five percent in early trading Thursday morning.

The report itself was favorable. Google’s cloud revenue surged 85%, year over year, to $24.8 billion, an astounding rate at such scale and higher than expected. The cloud business now has a remarkable backlog of business of $514 billion. Google CEO Sundar Pichai noted that the use of “tokens,” the unit of currency for AI, rose by 40%, quarter over quarter, to 22 billion tokens per minute. And five hundred Google Cloud customers have now exceeded a trillion tokens in usage apiece in the past twelve months.

With shares of Micron Technology up 235%, year to date, at a recent $955.60, including more than doubling in the past ninety days, the question of how long a very strong DRAM and NAND flash market can last is one of the most interesting questions in the very hot AI chip market.

The question implicates shares of competitors Samsung Electronics, which have more than doubled this year, and SK Hynix, whose newly minted American Depository Receipts are down two percent from their first-day close at a recent $166.65; and NAND maker Sandisk, which is up an astounding 470%.

Three brilliant technology analysts dug into the details of what might continue to make Micron stock work. You don’t have to go through them because I’ve extrapolated and summarize the high points for you.

Once again, the tech trade is rebounding on Monday morning. Shares of many of the TL20 stocks to consider, all of which, just about, are linked to a AI, are on the march higher. Fiber-optics component maker Lumentum is one of the strongest, up 8% at $790.74. Sandisk is also doing well, up 6%. I don’t think there’s any special significance here, as I indicated in this morning's podcast. There is simply a reversal of the trade, a continued search for direction…

UBS MAKES THE CALL TO GO BOTH WAYS!

Among the many who are searching for direction in Street research this morning are UBS strategists John Talbott and Jonathan Carson, who offer two different stock screens. One screen is a guide to look for bargains in beaten-down names, the other one consists of suggestions for how to reposition oneself, assuming the recent tech sell-offs are some kind of lasting “reset” of stocks.

Sigh. Perhaps slightly more certain is life on LHS 1140b, a small planet forty-nine light years from Earth that has been found to have a helium-based atmosphere, and therefore might support life, as reported today in Science magazine by researchers at Harvard University…

SO MANY AI GIGAWATTS, SO MANY WAFERS

Meanwhile, back on earth, makers of semiconductor capital equipment, such as Applied Materials, Lam Research, and KLA are now actually in “correction territory,” according to Bernstein analysts Stacy Rasgon, David Dai and colleagues in a note this morning. Despite the correction, “The group is still up >80% year-to-date,” they note, “with heavily expanded valuations,” they observe.

The week ending July 17th was one of the worst weekly returns ever for the AI-heavy TL20 group of stocks to consider, down 10%, though still up 47% for the year.

This is not the beginning of the end, simply a cooling-off of what had been a parabolic move upward.

There are a lot of explanations. The folks at Citrini Research contend that investors just don’t get how important AI is.

Bloomberg is talking about how the latest breakthrough Chinese AI model, “Kimi K3” from Chinese startup Moonshot AI, is the source of market panic.

Fact is, there will steadily be a commoditization of technology that has been touted as miraculous by OpenAI, Anthropic, SpaceX, etc., but can be replicated fairly easily.

Shares of Taiwan Semiconductor are trading down in Thursday pre-market trading by 4% at $402.22 despite a very robust outlook from the company overnight.

As I wrote on Monday, the revenue for the June quarter was already known, so the issue at hand was the forecast for the rest of this year and beyond.

My sense is the stock is down because of another big increase in spending, which is a good thing and a bad thing.

Shares of the entire AI trade are falling hard today, including a 9% drop in Micron Technology stock, and one possible explanation is a report late Tuesday by Reuters’s Max Cherney stating that CoreWeave, the neo-cloud computing provider, has been talking with bankers about ways to hedge against a decline in memory-chip prices, citing unnamed sources.

“AI cloud computing company CoreWeave is exploring the use of financial derivatives as a potential hedge against a future drop in memory and storage chip prices,” writes Cherney.

Cherney relates that CoreWeave is locked into pricing agreements with Micron — something I don’t believe either company has actually disclosed — and that CoreWeave wants to make sure it has a way not to overpay if memory prices drop. For that reason, relates Cherney, CoreWeave is considering, among other things, use of puts, contracts that would allow CoreWeave to sell its contracted chips if memory prices drop below the contract price down the road.

Shares of IBM are down 23% in Tuesday morning trading at $224.91, after the company preannounced the June quarter’s revenue and profit below consensus as a result of mainframe sales being hit by a shift in customer spending to servers, storage and memory chips — all the things that are being consumed in massive quantities to fund the AI buildout.

Regarding ASML’s report tomorrow morning of its June-quarter revenue and profit, Jefferies & Co.’s Jenardan Menon relates to clients today that “it feels as if there is an awful lot riding on tomorrow,” observing that “if ASML cannot increase its shipments, then TSMC [Taiwan Semi] cannot raise capex [capital spending], and Applied materials and WFE [semi equipment] expectations will be difficult to achieve, etc., etc.”

Shares of data center operator Terawulf are down 7% Tuesday at $19.22, and other AI data center names are being hit hard as well, after New York State governor Kathy Hochul Tuesday signed an executive order pausing for a year any construction of data centers in New York of fifty megawatts or larger while the potential effects of the data centers can be studied.

We’re heading toward earnings reports this week for ASML and Taiwan Semiconductor, two of the most consequential names of the AI trade, and that happens amidst a tug of war between deepening skepticism over AI investments and continued positive trends for companies such as Micron Technology and SanDisk that serve the AI trade.

Shares of the heavily AI-influence TL20 group of stocks to consider rose 4% for the week ended Friday, July 10th, a recovery from two weeks of selling prior to that.

For the month of July, the TL20 is up 2% through Friday’s close, and up 64% for the year — way better than the 3% decline this month of the Nasdaq Composite Index and the 13% gain of the Nasdaq thus far this year.

Ahead of Taiwan Semiconductor’s quarterly report on Thursday, the key number has, as usual, already been disclosed in TSM’s monthly sales report overnight. As usual, it’s above expectations.

Taiwan Semi’s June sales rose 68%, putting the quarterly total, $1,270 billion, in New Taiwan dollars, ahead of Street consensus for $1,254 billion.

Remember that April’s report, though very strong, saw the stock weak because management didn’t raise TSM’s outlook for its capital spending this year, causing some concern the business might not be as white hot as it has been.

So, the issue is really not the quarter but outlook for the second half of this year, as Wedbush analyst Matt Bryson points out in a note Monday: “The question in our view is how much can TSMC potentially exceed current 2H expectations (with any shortfall unlikely in light of the strong demand backdrop),” he writes.

Some of the parties that have been software’s strongest defenders amidst the threat of AI destroying software are starting to throw in the towel.

Jackson Ader of KeyBanc on Wednesday cut his rating on shares of Salesforce to Sector Weight from Overweight, and he reflects back on the vigorous defense of software he’s been carrying on since August.

Ader had previously argued the biggest software firms such as Salesforce were too big to be replaced by new stuff cobbled together with AI.

But, he relates, customer feedback is not good for Salesforce. “We attend more Salesforce partner and customer events than any other company in our coverage, and feedback from those customers has been consistent in two ways,” writes Ader. “1) customers' data is not in order to do meaningful AI work; and 2) Agentforce, as a product, just isn't there.” He’s referring to Salesforces offering for “agentic AI” to automate tasks such as sales prospecting.

I’m not surprised this is turning out to be a dud.

If you read through the 398-page prospectus for the expected offering Friday of American Depository Shares of SK Hynix, the Korean maker of DRAM and NAND, you will be struck by the lack of important information.

Hynix is the second-largest memory-chip company after Samsung Electronics, also based in Korea, and ahead of Kioxia (a spin-out of Japan’s Toshiba), Micron Technology and SanDisk. Hynix is also the top maker by revenue of “high-bandwidth memory,” HBM, currently the cutting edge of DRAM that is crucial for AI applications.

The company already has common shares listed on South Korea’s Kospi exchange. This $28 billion offering in the U.S. is meant to raise funds for the company’s factory expansion in Korea and China by tapping into the recent fervor for memory-chip stocks. Hynix’s ordinary shares are up 236% this year, slightly ahead of Micron’s 232% rise.

Given that Hynix is funding manufacturing expansion, what you would like to know from its prospectus, what’s crucial, is the shape of the global market for DRAM and NAND. That’s key because in a commodity industry, profit and peril rest on the control of supply to prevent over-supply situations.

Dear reader, how well I remember walking the streets of New York City on July 3rd, reporting on the many who waited hours or even days in line at an Apple Store or an AT&T shop to be the first to have the first iPhone.

Honestly, I had forgotten that it has been almost twenty years. And, apparently, the anniversary next July could be an unhappy one for Apple’s stock, according to Jefferies & Co.’s Edison Lee, who Monday cut his rating on Apple stock to Underperform from Hold.

Keep in mind, predicting disasters for Apple’s forthcoming products has proven very tricky for analysts.

Lee’s focus is the rumored “all-glass” iPhone model expected next year as a twentieth-anniversary celebration.

In case you have been under a rock, Bloomberg’s Mark Gurmanreported a year ago, and MacRumors’s Hartley Charltonstudiously summarized last week from that reporting, a description of an iPhone made of glass that “wraps around” all four sides of the device, something that sounds like a kind of “infinity pool” of a screen.